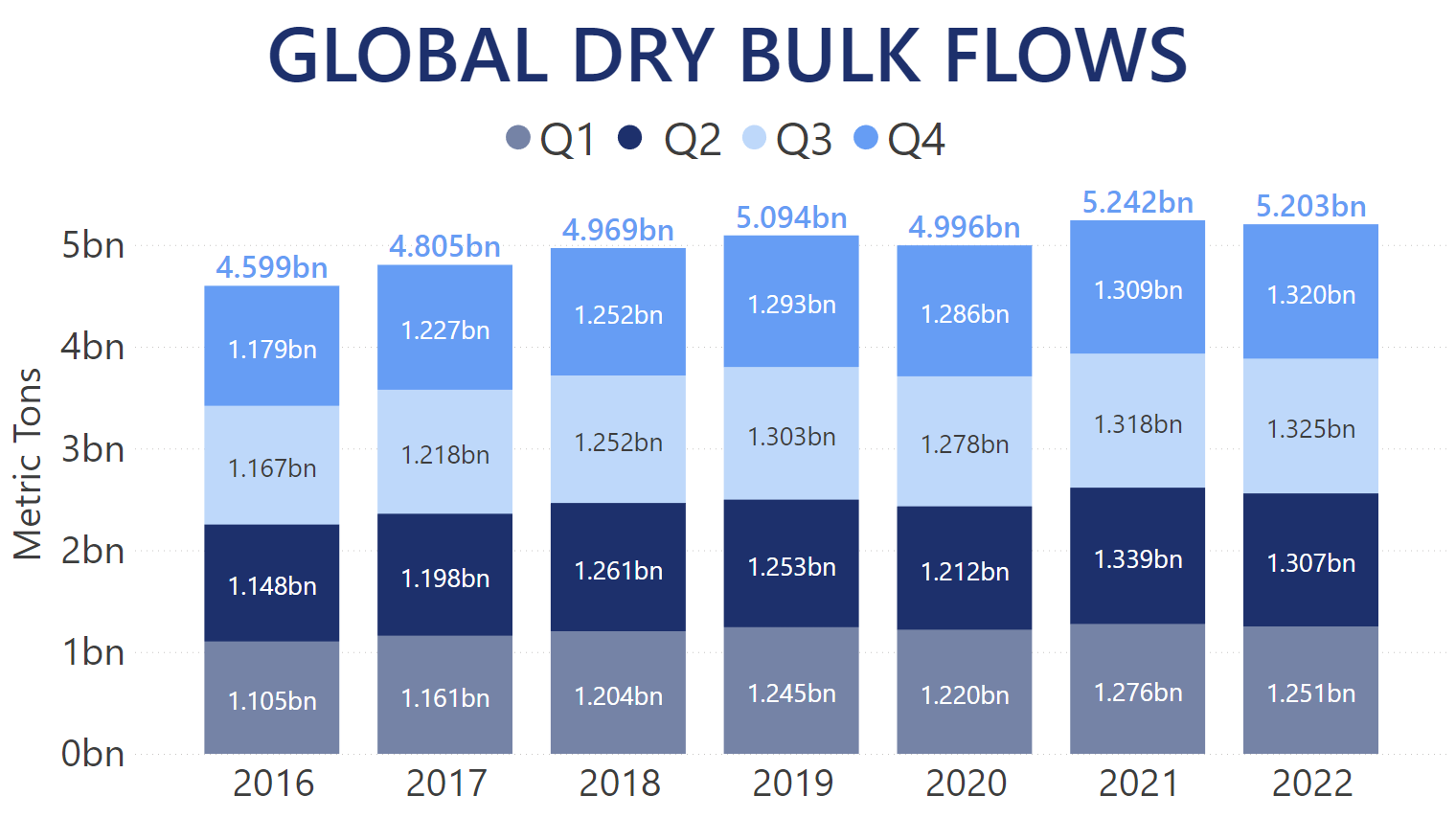

Global Dry Bulk seaborne trade saw just over 5.2bn MT of cargo shipped in 2022. This places last year as the second-highest ever in terms of quantities transported according to our Trade Flows data. Strong Q3 and Q4 performance meant that the last two quarters of 2022 set records, improving on 2021 levels by 0.5% and 0.8% respectively. However, the comparatively weak start of the year meant that 2022 came short by 0.7% year-over-year. In terms of laden voyages completed by Dry Bulk vessels, over 150,000 individual legs were carried out. This is 3% less than 2021 levels and signifies the shift towards the larger fleet segments last year, which we'll cover in more detail later in this article.

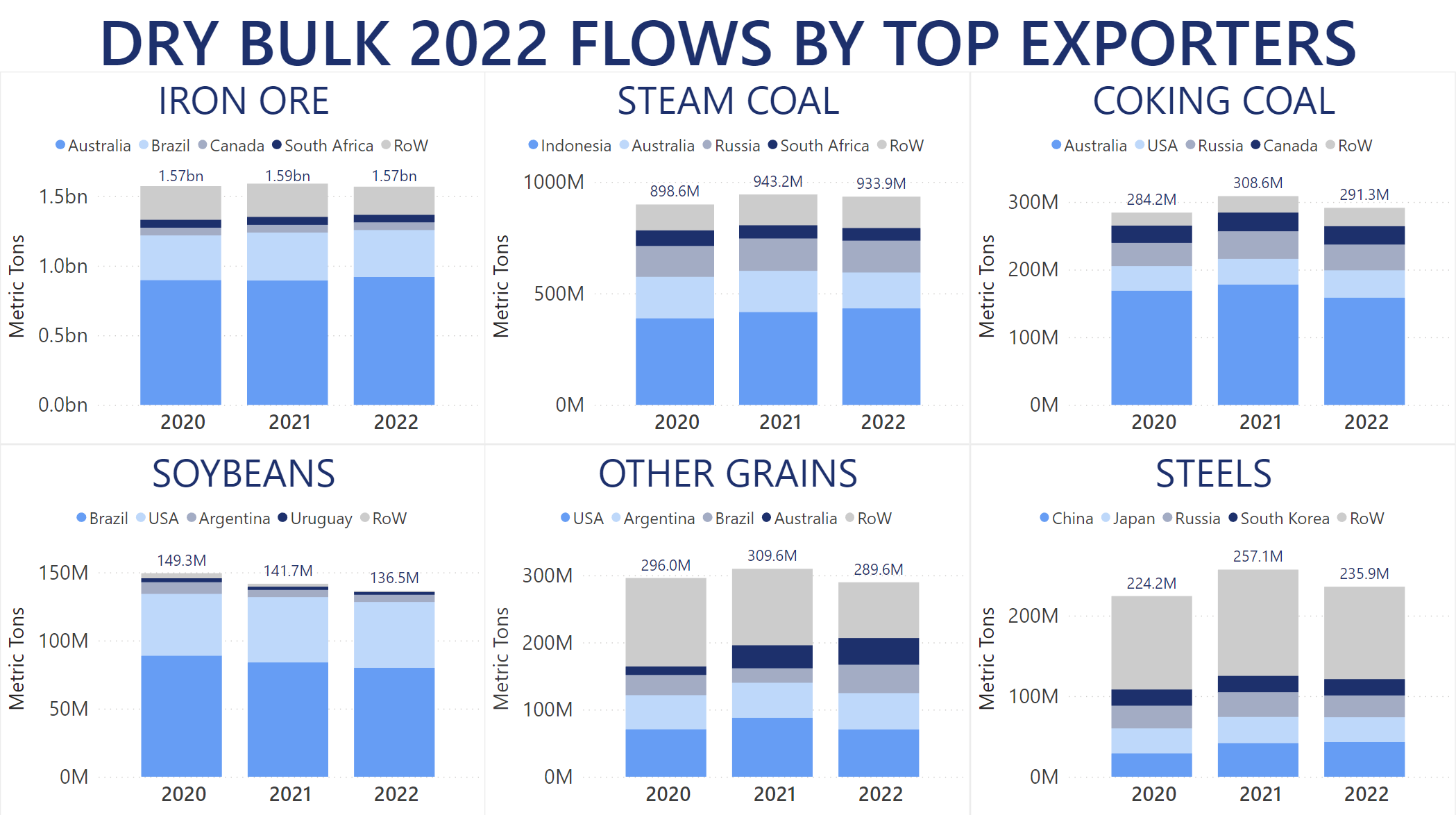

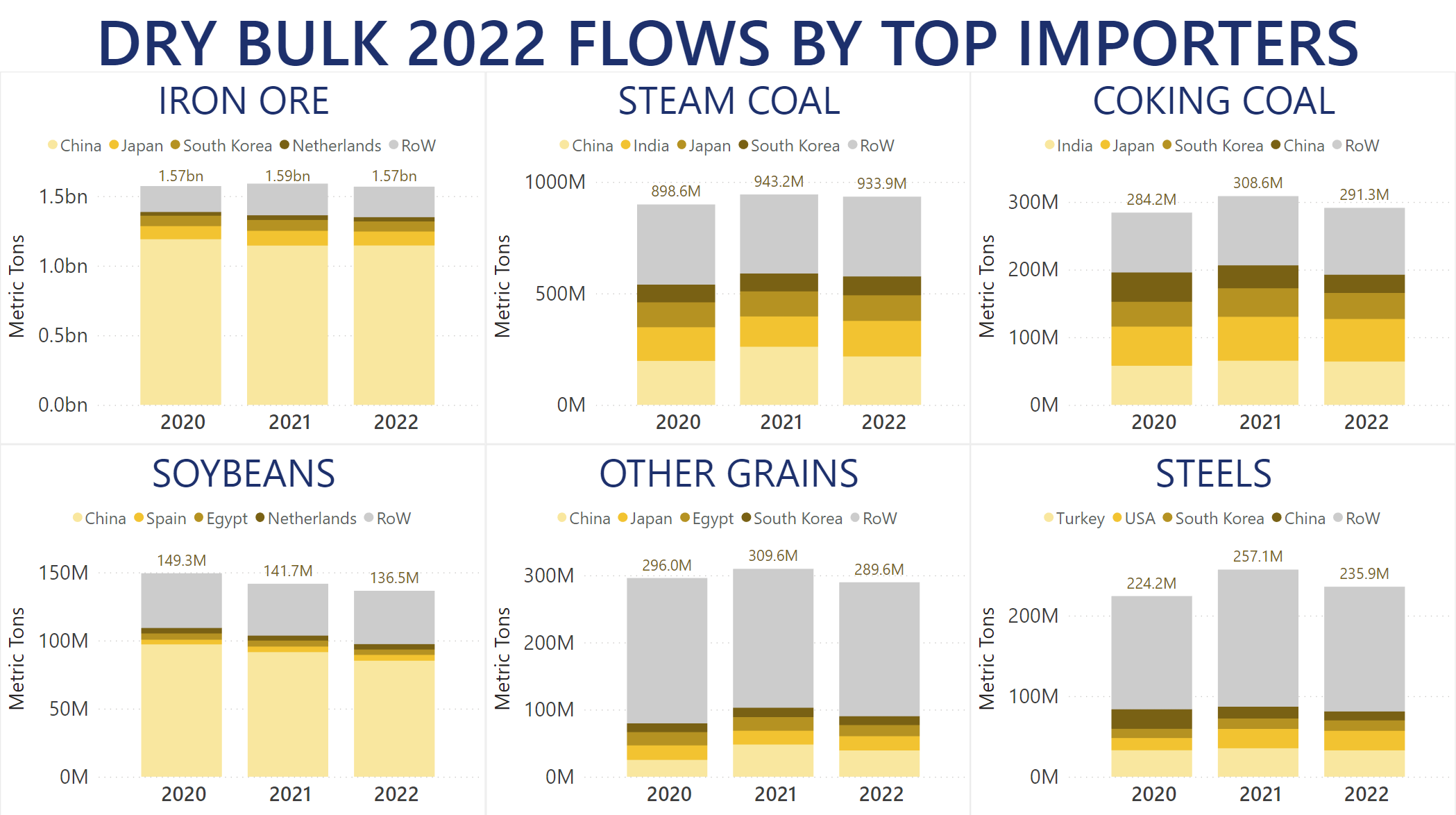

The year-over-year drop in 2022 Dry Bulk quantities was distributed almost universally across all major commodities. Iron Ore, the most common single Dry Bulk cargo carried by vessels worldwide, totalled 1.57bn MT in 2022 for a 1.3% year-over-year decrease. Supply-wise, the largest exporter of Iron Ore – Australia – actually increased its output in 2022, with just under 920m MT discharged across the globe for a 2.9% year-over-year boost.

However, this did not offset supply decreases by all the other major exporters. Brazil registered a 2.2% year-over-year drop, while South Africa was surpassed by Canada for the Top 3 spot in 2022, after shipping 6.3% less Iron Ore than in 2021. Another notable example in this market is Ukraine. Ranked as the 6th highest exporter of Iron Ore worldwide in 2021, the country ravaged by a Russian invasion saw its exports halt post-February, which translated into a 73.8% year-over-year drop in quantities and took over 18.7m MT of cargo off the market.

A similar trend could be observed in the Steam Coal market – the second-most common Dry Bulk commodity. At just under 934m MT discharged worldwide in 2022, this translated into a 1% year-over-year drop. Australia and South Africa shipped 13.2% and 5% less Steam Coal than in 2021, respectively. Indonesia, which is the largest supplier of this commodity, ramped up its Steam Coal deliveries by 4.1%.

Coking Coal shipments decreased by 5.6% year-over-year in 2022. Cargo originating from Australia totalled less than 158.5m MT, which is 10.9% less than 2021 levels. Meanwhile, the USA overtook Russia for the Top 2 spot, with the former increasing its exports of Coking Coal by 6.4%, while the latter saw its deliveries of this commodity drop by 6.8% year-over-year.

Soybeans saw a nearly universal decrease on their supply side, with Brazil shipping under 80m MT of cargo for the first time since 2019, translating into a 4.7% year-over-year decrease. The only major exporter of this commodity to ramp up its shipments in 2022 was the USA, which increased its seaborne supply of Soybeans by 0.8%.

Other Grain products also experienced year-over-year drops, with Corn quantities shipped decreasing by 4.8% year-over-year in 2022, while Wheat voyages transported 9.2% less cargo than in 2021. As with Iron Ore, Ukraine's supply was seriously hampered last year, decreasing the country's Corn shipments by 43.1% and Wheat – by 70.1% year-over-year. USA's Corn deliveries totalled just under 46.7m MT for a 22.2% year-over-year drop, while Brazil ramped up its seaborne output by 91.1% compared to 2021 levels.

Australia further increased its Wheat shipments in 2022, surpassing Russia as the world's largest supplier of the commodity, with over 24.5m MT of cargo shipped, translating into a 9.5% year-over-year boost.

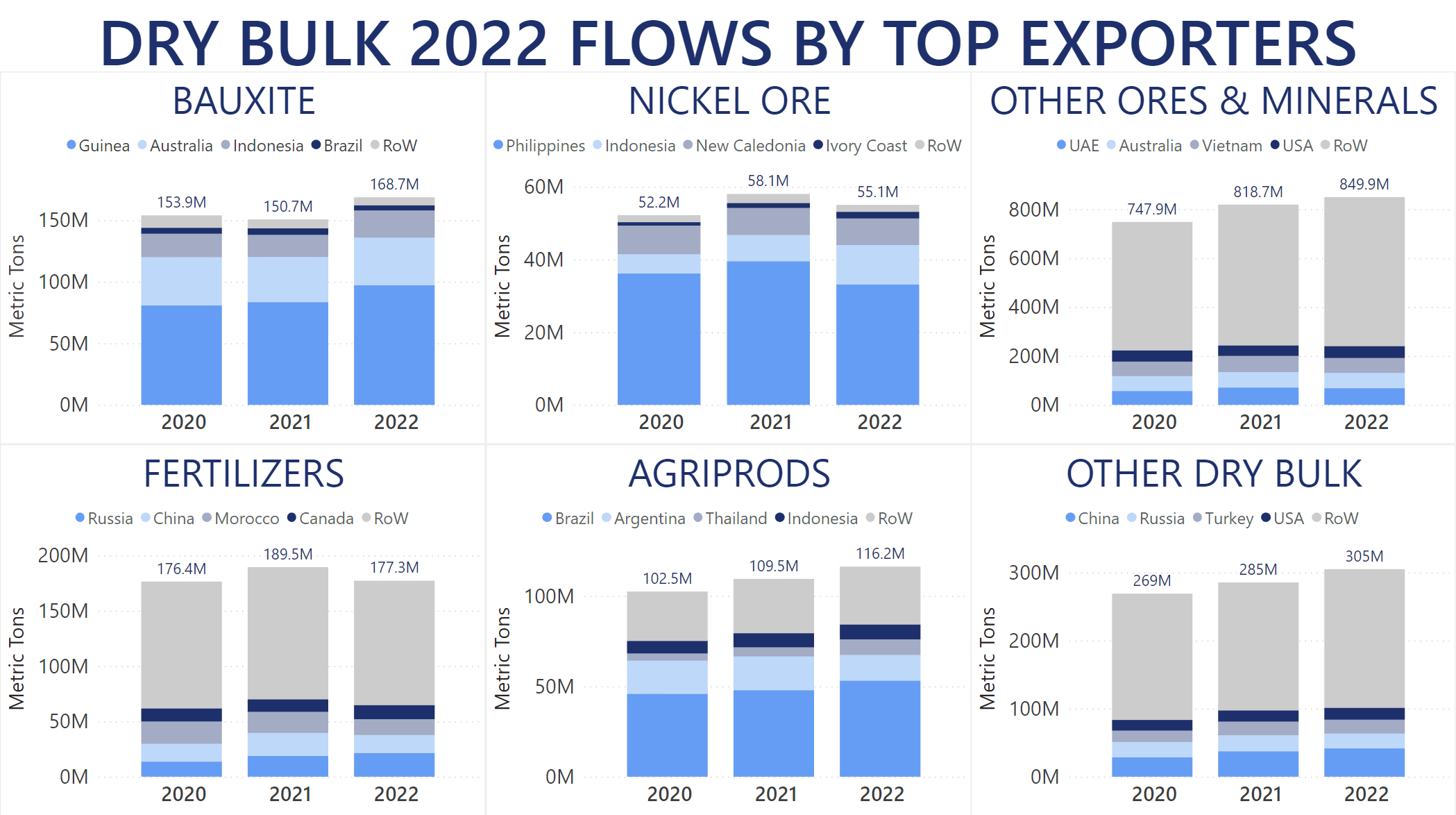

Bauxite turned to be a sort of a halo Dry Bulk commodity in 2022. One of the few exceptions to the general trend, cargo quantities increased by 12% year-over-year, with all major suppliers boosting their export levels. Guinea delivered over 97m MT of Bauxite worldwide for a 16.5% year-over-year gain. Australia's 38.7m MT translated into a 5.3% year-over-year increase, while 22.1m MT of Indonesian Bauxite was discharged across the globe for a 23.1% year-over-year boost.

Dry Bulk commodities, which are traditionally shipped in lower volumes, yet were traded at increased levels in 2022 include Wood Chips, Woodpulp, Pet Coke, Chrome Ore, Salt, Sugar, and Rice among others.

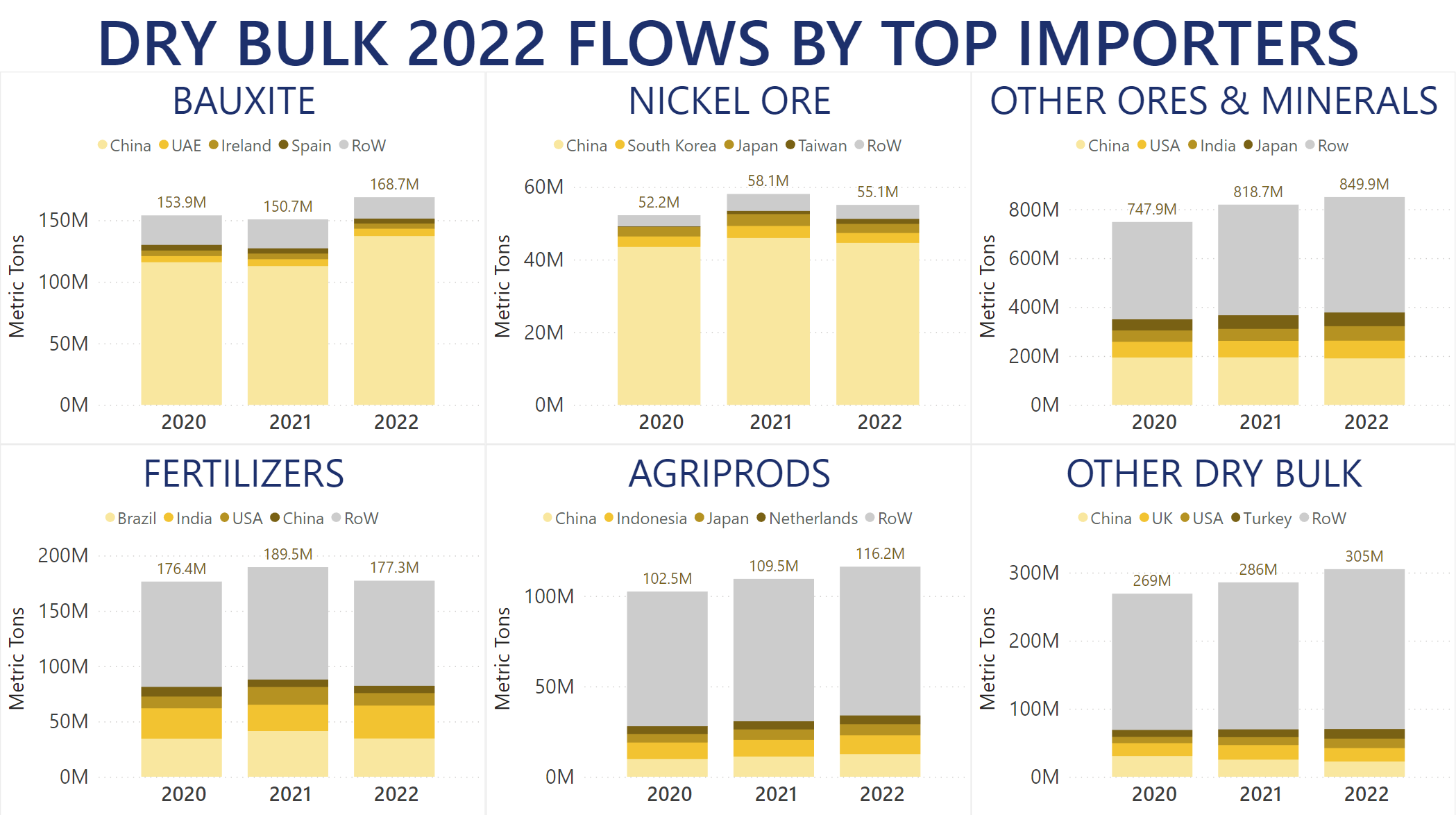

Demand-wise, overall Dry Bulk discharged in China dropped from over 2bn MT in 2021 to 1.95bn MT in 2022, reducing Chinese market share from 38.3% to 37.4%. As far as Iron Ore is concerned, however, China discharged a record-breaking 1,145m MT of cargo, for a 0.1% year-over-year increase. Nevertheless, demand from Japan dropped by 4.8% year-over-year, while South Korea imported 7.8% less Iron Ore than in 2022.

The trend in the Steam Coal market was on the opposite spectrum. Throughout 2022, India, Japan, and South Korea increased their seaborne imports of the commodity by 17.5%, 2%, and 5.3% year-over-year respectively. However, discharged quantities across Chinese ports decreased by 16.7% compared to 2021 levels, subtracting more than 43m MT of cargo out of the market.

In 2022, some European importers of Soybeans, such as Spain and the Netherlands, increased their demand for the commodity by 4.8% and 7.6%, respectively. Yet, China with its 62.4% market share was the trend setter. The largest importer of Soybeans discharged just over 85m MT – the lowest quantity since 2019 – for a 7% year-over-year decrease.

In the Steels market, South Korea moved into the Top 3 spot of importers in 2022 with just under 12.9 MT of cargo shipped to its ports. While on par with 2021 levels, demand from China and Vietnam dropped by 24% and 24.8% year-over-year, respectively. Meanwhile, Turkey – the largest importer of Steel products – had just over 32.7m MT of cargo discharged for a 7.3% year-over-year decrease.

Chinese imports of Bauxite in 2022 surpassed 137.1m MT for a 21.6% year-over-year boost. Other countries' demand for the commodity almost universally decreased, with Ukraine experiencing the most severe reduction of 81.9% year-over year and dropping out of the Top 3 spot it had in 2021.

In the Nickel Ore market, Taiwan took the Top 4 spot in quantities imported throughout 2022 after increasing discharges at its ports by 63% year-over-year. This was coupled with Ukraine being forced to decrease its Nickel Ore imports by 87.5% and Greece dropping its demand by 70.2%. China, as the major entity in this market, also reduced discharges of Nickel Ore by 2.9% year-over-year to under 44.6m MT.

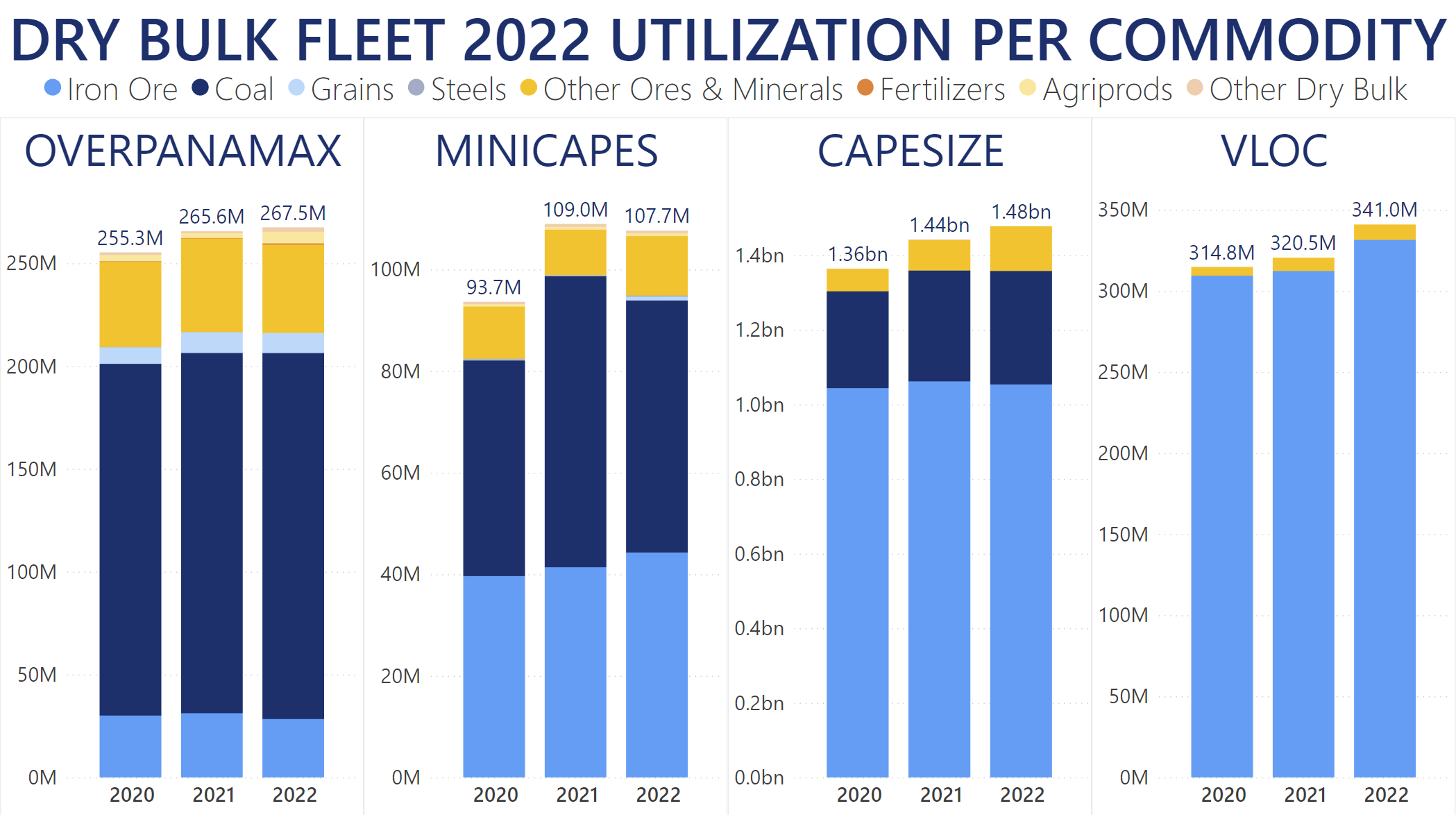

Fleet utilization by vessel size in 2022 almost universally favoured vessels above 68K MT of deadweight. Handysize and Handymax vessels up to 50K MT of deadweight combined carried 45.2m MT less cargo for a 5.8% year-over-year drop. The markets where the two smallest fleet segments experienced the most reduction in quantities transported were Coal (both Steam and Coking), Fertilizers and Grains.

Supramaxes between 50K and 60K MT of deadweight saw the largest drop in utilization percentage-wise, at 6.4% year-over-year. The vessels in this segment carried 52.2% less Iron Ore in 2022 than they had transported in 2021. Their use in the Coal, Grains and Steels markets was also decreased by between 8.4% and 10.8% year-over-year. As a silver lining for Supramax vessels, they were used for the shipping of 2.3% more Fertilizers and 3.5% more Agricultural Products year-over-year.

The biggest shift in trends in the Ultramax fleet segment between 60K MT and 68K MT of deadweight saw them carry 43.2% less Iron Ore last year than they had done in 2021. At just under 11m MT of this commodity transported, it meant that Ultramaxes were the least used vessels for the shipping of Iron Ore worldwide.

Panamax vessels between 68K and 85K MT of deadweight saw little shift in their utilization compared to 2021 data. Yet it is also the first fleet to see a marginal year-over-year increase, having carried over 920.8m MT of Dry Bulk. The largest portions of this were voyages carrying Steam Coal at over 329.5m MT and Soybeans at over 104.7m MT.

OverPanamax vessels between 85K and 100K MT of deadweight were also mostly used for Coal trades and carried a total of more than 267.4m MT of Dry Bulk commodities throughout 2022 for a 0.7% year-over-year increase. Meanwhile, the Minicapes fleet between 100K and 120K MT of deadweight was the only larger fleet segment to see a year-over-year drop of 1.2% after carrying about 7.7m MT less Coal cargoes in 2022.

As usual, Capesize vessels between 120K MT and 220K MT of deadweight carried the most Dry Bulk cargoes in 2022, with their combined shipments totalling just under 1.48bn MT for a 2.5% year-over-year boost. The majority of these included over 1bn MT of Iron Ore transported worldwide. While a 0.8% year-over-year decrease for this specific commodity, it still gave Capes a 67.4% market share in Iron Ore.

The VLOC fleet took the crown for percentage-wise performance in 2022. The largest vessels on the market transported about 6.4% more tonnage year-over-year, the vast majority of which was over 331m MT of Iron Ore. Bauxite shipped in VLOCs also increased by 15.9% compared to 2021 levels for a total of 9.5m MT.

Our Trade Flows tool allows you to follow each commodity, importer, exporter, fleet segment, and a lot more. You can gain accurate intelligence on a macro- and micro-level for the entire shipping industry. Book a demo below to see everything Trade Flows can do for you.